Worldwide public cloud end-user spending is expected to reach $332.3 billion in 2021 and over $397,4 billion in 2022. The fact that emerging technologies, such as edge computing and virtualization, enter the mainstream is an additional and increasingly important cloud spending driver. We can also expect more investments for complex and novel use cases whereby the usage/adoption of cloud computing and services is combined with IoT, 5G, AI, and other technologies.

Spending on public cloud services continues to grow at impressive rates. With the actions that organizations had to take to ensure business continuity in 2020, it probably isn’t a surprise that the COVID-19 pandemic was and continues to be an essential element in this regard with companies and individuals increasing digital adoption as illustrated in this article on ‘transformation for a new normal.’

In 2020, worldwide end-user spending on public cloud services reached around $270 billion, and it doesn’t look as if things will slow down in 2021 and 2022.

On the contrary, the pandemic increased the interest of CIOs in the cloud, and it’s clear that the doubts concerning moving (critical) workloads from on-premises to the cloud weren’t as present in 2020 as they used to be for all the obvious reasons.

“Cloud will serve as the glue between many other technologies that CIOs want to use more of, allowing them to leapfrog into the next century as they address more complex and emerging use cases” (Sid Nag, VP Analyst, Gartner)

The pandemic and, along with it, the experiences regarding public cloud migrations and changed attitudes certainly aren’t the only drivers. In fact, per Gartner, emerging technologies such as containerization, virtualization, and edge computing are becoming mainstream and important drivers of additional cloud spending. Of course, the pandemic had an ‘accelerating impact’ on some of these technologies as well (think edge in manufacturing, for instance).

Worldwide public cloud end-user spending: fundamental shifts and essential data

According to Gartner, worldwide public cloud end-user spending will grow 23 percent in 2021 (to a total of $332.3 billion) and reach around $397,5 billion in 2022.

Throughout this forecast period, the effect of some drivers will change. However, the mentioned impact of containerization, virtualization, and edge computing becoming mainstream is a stayer.

Edge spending is on the rise as we move to a hybrid distributed environment (ideally dictated by use cases and with industries such as manufacturing, professional services, and retail business leading for now) where cloud becomes the new core, and edge is crucial to power the next digital transformation wave.

Gartner’s research vice president Sid Nag explicitly points to the three mentioned emerging technologies. As far a the pandemic’s impact is concerned, he states that even “absent the pandemic, there would still be a loss of appetite for data centers,” with “the pandemic serving as a multiplier for CIOs’ interest in the cloud”.

The impact of the pandemic, for now, is higher than – hopefully – in the years ahead when the usage and adoption of cloud will evolve to combine cloud with technologies such as artificial intelligence, 5G, and IoT (Internet of Things).

At the same time, use cases in areas such as infrastructure and application migration will relatively increase slower. In other words: more complex use cases and the integrations which are essential in so many areas such as Industry 4.0 as one technology rarely is enough.

“Emerging technologies such as containerization, virtualization and edge computing are becoming more mainstream and driving additional cloud spending” (Sid Nag, VP Analyst, Gartner)

Sid Nag: “cloud will serve as the glue between many other technologies that CIOs want to use more of, allowing them to leapfrog into the next century as they address more complex and emerging use cases. It will be a disruptive market, to say the least.”

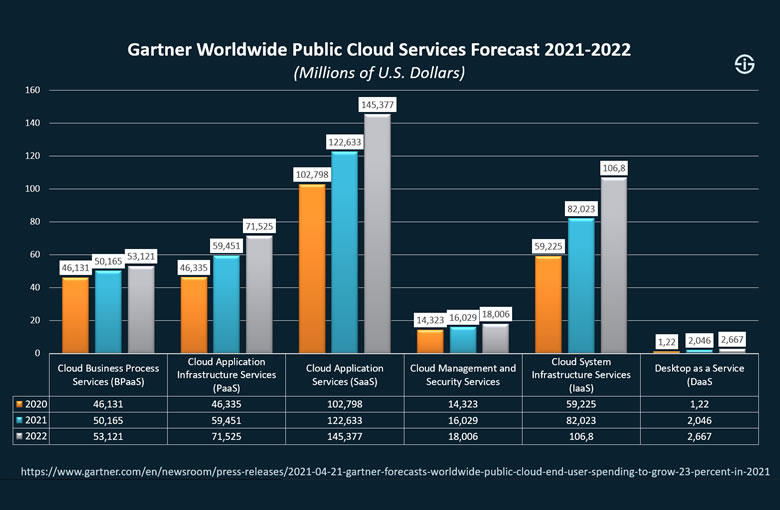

Looking at the public cloud services market a bit more in detail, Software as a Service (SaaS) remains the largest public cloud computing segment and at the same time is changing with “the demand for composable applications requiring a different type of SaaS experience.” Gartner also stresses the vital role of SaaS-based applications in the context of COVID-19 vaccination.

While spending on SaaS is forecast to reach $122.6 billion in 2021, Infrastructure-as-a-service (IaaS) and desktop-as-a-service (DaaS) are expected to see the highest growth in 2021, with 38.5% and 67.7%, respectively.

Here, continued pressures to scale infrastructure to support the movement of complex workloads to the cloud and the changing demands of a hybrid workforce are essential.