Blockchain technology was “invented” to circumvent the need of a central authority in cryptocurrency Bitcoin. The decentralized database and ledger technology has moved past that stage and is gaining traction in an increasing number of applications and digital transformation in sectors such as banking and insurance.

Is there anything that blockchain technology isn’t going to change? According to its many believers it will change a whole lot and we’re just in the very early days. Given its roots and inherent characteristics, the possibilities of blockchain in finance are explored and increasingly applied in financial technology (FinTech) with applications in banking, insurance and more financial services, including entirely new models of paying for and securing transactions of the financial kind.

Some strong advocates, such as Don Tapscott, even call blockchain technology, a Distributed Ledger Technology (DLT), a bigger deal than the Internet. And, if you happened to have been there in the early days of the Internet, imagine we’re more or less in the 1990s when Yahoo was founded and for many almost a synonym of the Web. So, really early days.

Others have more moderate views on the potential of blockchain and in some domains think it won’t be that useful at all. That’s what happens in early days. Yet, its clear that blockchain technology is important and not just in finance, the topic of this article. After all, transactions happen in many forms, shapes and areas. To name one: IoT (the Internet of Things) where IoT and blockchain are a fit for many reasons. And there is more, much more. A look at blockchain with a focus on financial technology, banking, insurance and finance overall.

The huge expectations regarding blockchain technology’s potential

The truth about blockchain? It will be big, it’s going to affect your industry and life but no one really knows exactly in which domains and precisely how. That’s the reason why many IT firms are not really talking too much about it: we are at the start of the blockchain technology hype cycle but you better watch the essence in several years to come as some very serious companies and organizations are diving deep into the possibilities and launching numerous highly funded initiatives.

Blockchain can speed up the settlement times of many payments transactions

If you landed on this page you want to know what blockchain technology is and what it can do. Maybe you stumbled upon a news article telling how blockchain will solve cybercrime, change music rights management, transform identity management, reshape the ways we conclude legal contracts, transform voting or, most often mentioned in a context of fintech, alter many aspects of financial services, from payments to share purchases and changing financial service infrastructures. A lot of expectations, possibilities, initiatives (in each of the above mentioned domains and more) and digital transformation indeed.

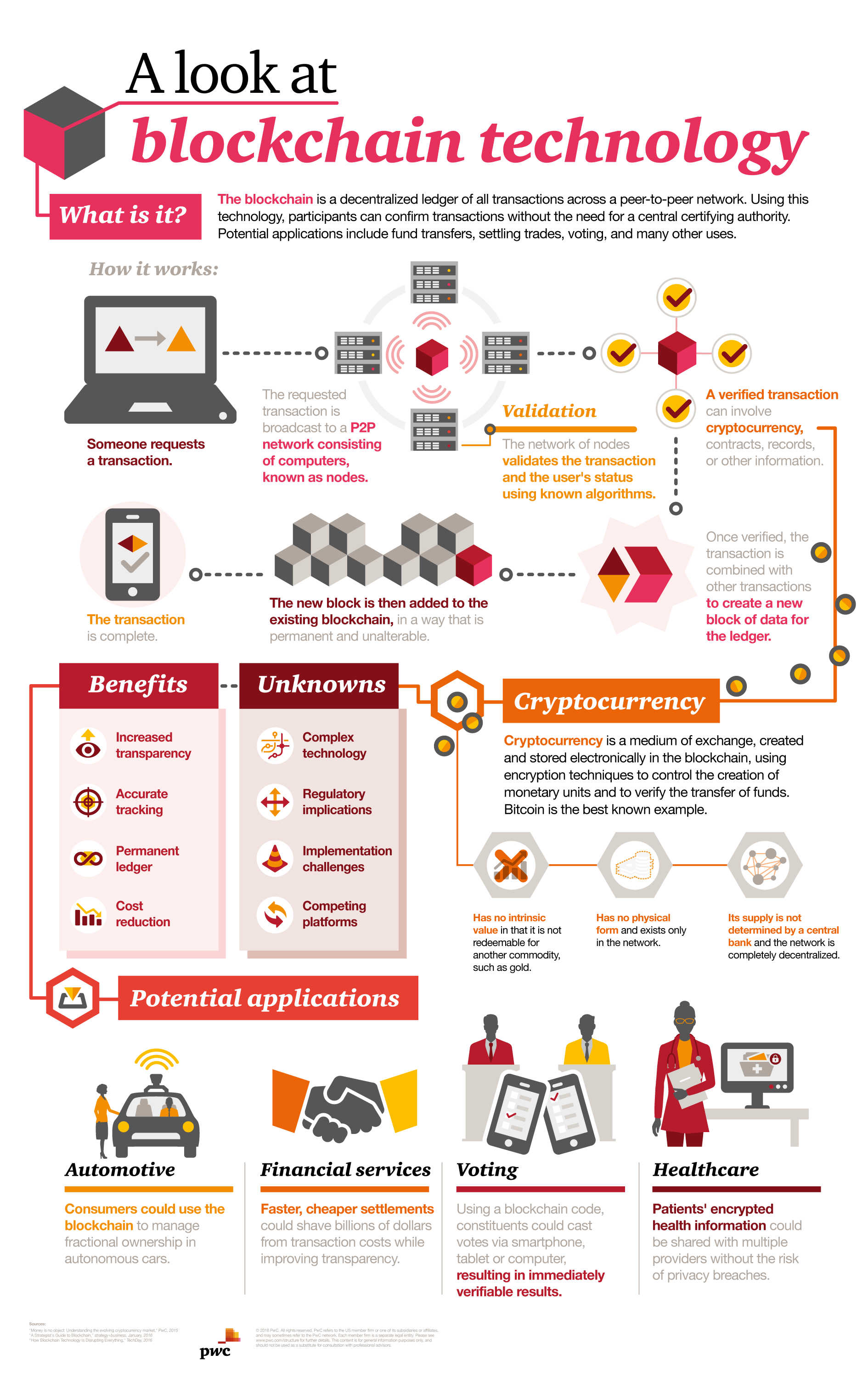

Blockchain: a decentralized ledger of all transactions across a peer-to-peer network

The current predominant link with finance (with a lot of testing and investing going on as well) is the reason why blockchain technology is often categorized under financial technology or fintech. That also has a lot to do with the fact that blockchain powers Bitcoin, the famous virtual currency or cryptocurrency. In this stage that’s normal and it leads to confusions. Expect the link with Bitcoin and others to gradually dissapear.

Multiple issues and challenges facing the development and deployment of blockchain technology need to be addressed, including questions about scale, reliability, and regulation (IDC)

Blockchain technology is not a financial technology. It’s a database. Or better: a decentralized/distributed database which serves as a (public, in the case of virtual currency) online ledger keeping record of transactions that can’t be changed. In this overview and given, current market realities, we’ll mainly cover it from the fintech perspective though (with more applications mentioned, among others in the video below).

Blockchain is indeed being debated and looked upon from numerous perspectives as you could already see in the examples in our introduction. It has gone beyond the world of finance (even, if, again, it’s really very present there). There are even clear cases to bring blockchains to the Internet of Things. Maybe one day we’ll only know it as DLT, short for Distributed Ledger Technology, as initiatives beyond finance continue to grow and some will prefer to remove the link with Bitcoin. Again, we can’t stress this enough, blockchain is still in its early days and many uncertainties, questions and concerns still exist.

Back to the esssence of the underlying technologies and principles. Each business has a ledger, containing all records on transactions: purchases and sales, managed by the finance department. When a transaction happens, for instance paying another business, there is an intermediary who validates it. In payments this is, for instance, a bank. The blockchain removes the need of such an intermediary or better: replaces the intermediary with a (peer-to-peer) computer network. Blockchain can, as such, speed up the settlement times of many payments transactions.

One can question if it’s always a good idea, let alone useful and worth the while, to remove intermediaries. Moreover, trade is about more than transactions. That’s exactly where a lot of debate exists, potential and real application per potential and real application. These debates sometimes tend to get almost a little political and emotional, even “religious” in some cases. The world of blockchain technologies excites many, also people who definitely want to change everything. We won’t elaborate on all those discussions here (maybe in a later, more in-depth piece or paper) but do keep that aspect in mind when setting out to learn more on blockhain (in fact, multiple blockchains in reality). It all again shows we’re still in the beginning.

For the fans of hype cycles: according to Gartner’s Hype Cycle for Emerging Technologies, 2016, blockchain is still an innovation trigger and reaching the peak of inflated expectations (read article on Forbes, August 29, 2016). We think it might still take some time before it actually does.

How does blockchain technology work?

Each stage of a transaction is generating a set of data which are called blocks. As the transaction progresses, more blocks get added, forming a chain, hence the name.

Despite its apparent complexity, a blockchain is just another type of database for recording transactions – one that is copied to all of the computers in a participating network.

Just as in cryptocurrencies like Bitcoin and others, which are based on blockchain technology, encription software guarantees no one can ever delete or change blocks.

Several computers across a network have the blockchain software installed. Each transaction is shared to these nodes in the network and they compete (in Bitcoin jargon ‘mining’) to verify the transaction. The first one that verifies it also adds the block of data to the chain and gets an incentive for being first. The other nodes next check the transaction, agree that it’s correct and replicate the record. All the computers then keep an updated copy of the ledger, and this acts as a form of proof that the transaction occurred.

As said, blockchain relies on peer-to-peer agreement as opposed to a central authority to validate a transaction. Until now, if you wanted to make a transaction, you informed a central authority who checked the details with everyone involved and holds a central record such as a bank, a notary or any other central certifying authority. In the blockchain model there is no such central authority. Transacting parties rely on an open register, the ledger, to validate the transaction. Authority comes from the fact that numerous computers, ‘miners’, have looked at the broadcast data, checked it and found it correct. Trust comes not from a notary’s stamp, but the presumption that those computers can’t all be wrong. You can imagine that there is quite some discussion here as well.

Some benefits of blockchain technology

In the blockchain model there is no central authority. Transacting parties rely on an open register to validate the transaction.

Speed

The absence of a central authority in theory makes blockchain faster. If you’re relying on a central certifier, you depend on limited resources. Clearing and settling stock trades, for instance, can take days and usually involves some human intervention. With blockchain you have lots of computers competing to process your transaction as quickly as possible. Today they can do it in a matter of minutes. In the future it may only take seconds.

Cost

Blockchain is also cheaper. All the computers holding the blockchain are paid for by the participants in the hope that they will earn the incentive for being the first to validate the transaction.

Transparency

Blockchain is more transparent. It can give regulators and compliance officers clearer insight into the provenance of financial transactions, helping them to combat money laundering and manage risk.

Tracking

As nothing can be changed and the ledger is present across multiple nodes, blockhain is easier to track.

The technology, benefits and unknowns visualized

Pwc has a good easy explainer and a visual in case you’re new to blockchain.

As the infographic shows, the company defines the blockchain as a decentralized ledger of all transactions across a peer-to-peer networks, enabling participants to confirm transactions without the need for a central certifying authority. The infographic also explains the process well and gives some examples of applications of blockchain technology.

Blockchain technology beyond finance

As the blockchain ecosystem evolves and different use-cases emerge, organizations in all industry sectors will face a complex and potentially controversial array of issues, as well as new dependencies.

As promised we were also going to touch upon the various possibilities that are being looked at regarding blockhain as we speak. It’s impossible to tackle them all and it’s certainly impossible to write a definitive guide or something similar on the future or potential of blockhain. Some authors and many researchers have delved deep into the matter already but as tends to be the case with the future nothing is sure and no one can write that definitive guide in this stage, if ever at all.

- Quotes IDC, press release: Blockchain Technology: Disruptive Forces in Financial Services (20 Jun 2016).

- Quotes Deloitte: Blockchain. Enigma. Paradox. Opportunity.

Top image: Shutterstock – Copyright: Montri Nipitvittaya – All other images are the property of their respective mentioned owners.